Suzanne Dyer

Phone

(310) 528-7480

Email

[email protected]

Short-term rentals (STRs), sometimes referred to as short-term vacation rentals (STVRs), have become one of the most talked-about real estate strategies in recent years. Beyond their income potential, STRs offer unique and often misunderstood tax advantages that can significantly improve an investor’s after-tax returns. At the same time, regulatory rules vary widely by city, especially along the California coast, making it critical to understand where STRs are legally permitted.

In the South Bay, two coastal cities frequently assumed to be “off limits” for short-term rentals are Manhattan Beach and Hermosa Beach. In reality court rulings and coastal regulations have opened the door to legally operating STRs in specific zones within both cities, provided owners follow the rules.

This blog breaks down:

The key tax advantages of short-term rentals

Why STRs can be more tax-efficient than long-term rentals

Where short-term rentals are currently allowed in Manhattan Beach and Hermosa Beach

What buyers and owners should understand before investing

One of the biggest tax advantages of owning any rental property is depreciation. The IRS allows residential rental property to be depreciated over 27.5 years, even though the property itself may be appreciating in value.

Depreciation is a non-cash expense, meaning you can deduct it from your income without writing a check. This often allows STR owners to generate positive cash flow while reporting little or no taxable income from the property.

Short-term rentals are especially well-suited for cost segregation studies. A cost segregation analysis breaks a property into components with shorter depreciation lives, such as flooring, fixtures, appliances, cabinetry, and certain electrical and plumbing elements.

This allows owners to accelerate depreciation into the first several years of ownership, potentially creating significant paper losses early on. For higher-income households, this can be an extremely effective tax planning tool when done correctly and documented properly.

This is where short-term rentals differ dramatically from traditional long-term rentals.

Long-term rentals are typically classified as passive activities, meaning losses are often limited and cannot offset W-2 or business income unless certain thresholds are met.

Short-term rentals, however, may qualify as non-passive if:

The average guest stay is seven days or less, or

The average stay is 30 days or less and substantial services are provided, and

The owner materially participates in the activity

When structured properly, this means losses from a short-term rental may be used to offset active income, such as salary, commissions, or business income. This distinction alone is one of the biggest reasons STRs are attractive to professionals and entrepreneurs.

Unlike long-term rentals, short-term rentals are typically fully furnished. This creates additional deductible expenses, including:

Furniture and décor

Beds, mattresses, and linens

Electronics and smart home technology

Kitchenware and small appliances

Many of these items can be depreciated over shorter timeframes, further accelerating deductions.

STR owners may deduct ordinary and necessary expenses related to operating the property, including:

Mortgage interest and property taxes

Insurance

Utilities and internet

Cleaning and turnover services

Repairs and maintenance

Property management fees

Marketing and platform fees

Accounting and legal costs

When managed properly, these expenses can significantly reduce taxable income.

In certain cases, short-term rentals may qualify as a trade or business for tax purposes, making the owner eligible for the Qualified Business Income deduction. This can allow up to a 20 percent deduction on qualified income, depending on income levels and structure.

In many situations, rental income is not subject to self-employment tax, even when classified as a business for loss purposes. However, providing hotel-like services can change this treatment, making professional tax guidance essential.

Short-term rentals can also play a role in long-term wealth planning. Properties held until death may receive a step-up in basis, potentially eliminating capital gains for heirs. STRs can also be held in LLCs or trusts to align with broader estate planning strategies.

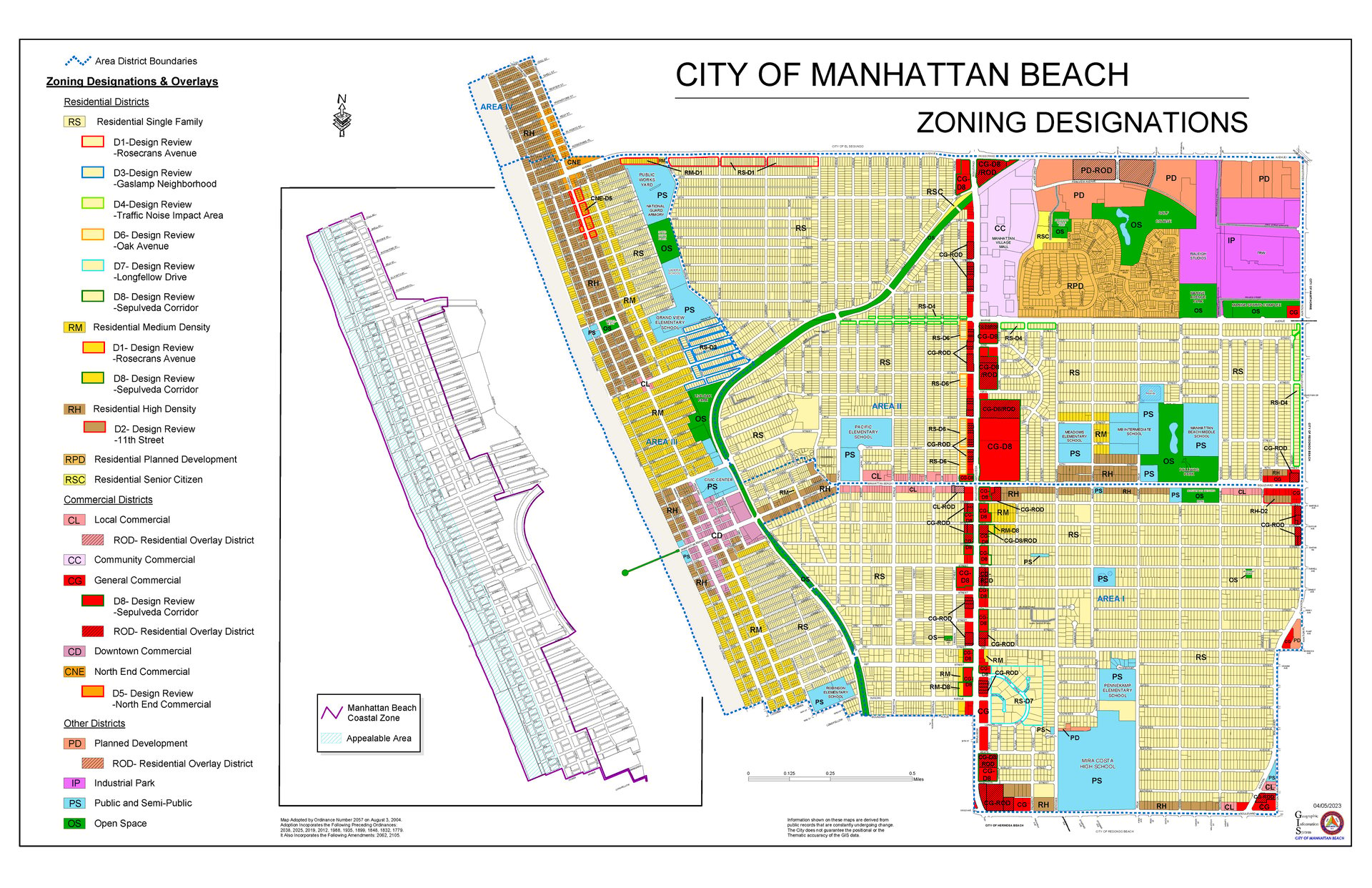

Short-term rentals are not banned citywide in Manhattan Beach, despite common misconceptions.

Following a 2022 Court of Appeal decision, Manhattan Beach’s ban on short-term vacation rentals does not apply to properties located within the Coastal Zone. As a result, STRs are permitted within the Coastal Zone, subject to compliance requirements.

Short-term rentals of fewer than 30 days remain prohibited in most residential areas outside of the Coastal Zone.

Owners operating short-term rentals in permitted areas must:

Obtain a business license

Collect and remit Transient Occupancy Tax (TOT)

Comply with all applicable city regulations

Understanding whether a specific property falls within the Coastal Zone is critical before purchasing with STR use in mind.

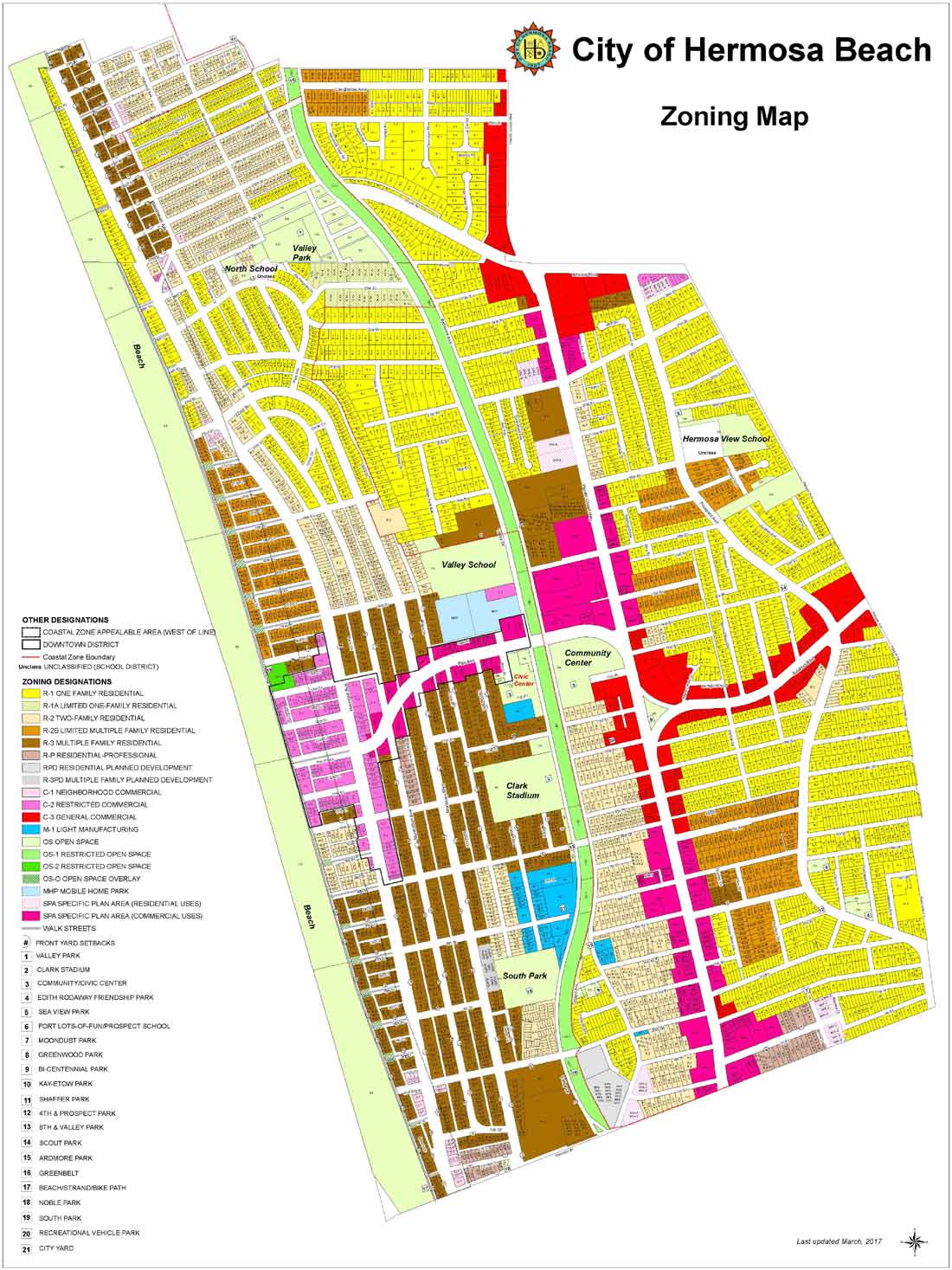

Hermosa Beach has also evolved in its treatment of short-term rentals.

Short-term vacation rentals are permitted in specific zones, including:

C-2

C-3

SPA 7

SPA 8

SPA 11

These zones generally include certain commercial and nonconforming residential areas.

Similar to Manhattan Beach, court actions have limited the city’s ability to enforce a blanket ban within the Coastal Zone. A regulated program exists, and in 2025 a preliminary injunction stopped enforcement of the ban in certain coastal cases.

Hermosa Beach requires:

A short-term rental license

Compliance with city regulations

Rentals defined as stays of fewer than 30 consecutive days

The tax advantages of short-term rentals are only meaningful if the rental is legally operated. Buyers considering STRs in Manhattan Beach or Hermosa Beach must:

Confirm zoning and Coastal Zone boundaries

Understand permitting and licensing requirements

Factor in Transient Occupancy Taxes

Stay current on evolving regulations and court rulings

This is where experienced local guidance matters. Not every property is suitable for STR use, and mistakes can be costly.

Short-term rentals offer a compelling combination of income potential and tax efficiency when structured correctly. Through depreciation, accelerated write-offs, potential active income offsets, and fully deductible operating expenses, STRs can significantly outperform traditional long-term rentals on an after-tax basis.

At the same time, cities like Manhattan Beach and Hermosa Beach demonstrate that STRs are not simply allowed or banned. They are regulated, nuanced, and highly location-specific. Buyers who understand both the tax strategy and the regulatory landscape are best positioned to succeed.

For investors, second-home buyers, and homeowners exploring income opportunities along the coast, short-term rentals can be a powerful tool when approached thoughtfully, compliantly, and with expert guidance.

Suzanne Dyer

Luxury Real Estate Specialist

Strand Hill | Forbes Global Properties

Over 1 Billion Dollars in Career Sales

Top Realtor in Palos Verdes and the South Bay

310 528 7480 | [email protected]

DRE 01054310

If you´re listing or selling real estate in the Palos Verdes Peninsula and surrounding areas, put a winning real estate professional to work for you.

Let's Connect